Why SuperDiversification works is demonstrated step-by-step.

In this section, we demonstrate why SuperDiversification works. Click on each of these steps, or scroll down the page:

» Because diversification works…

» SuperDiversification works better.

» SuperD seeks to take only the risks you get paid to take.

» Why seven asset classes? The SuperDiversifiers are often front-runners…

» Yet they can lower risk.

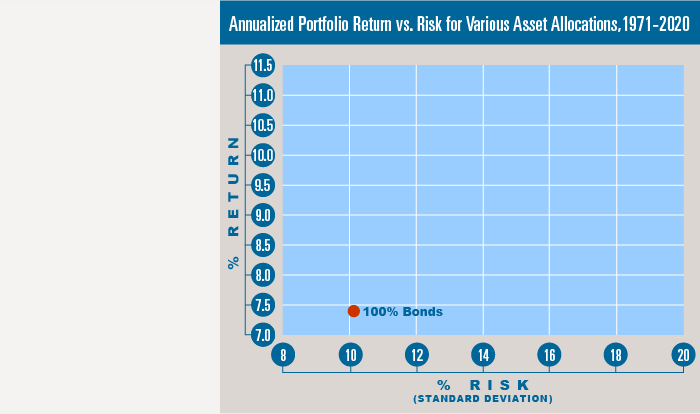

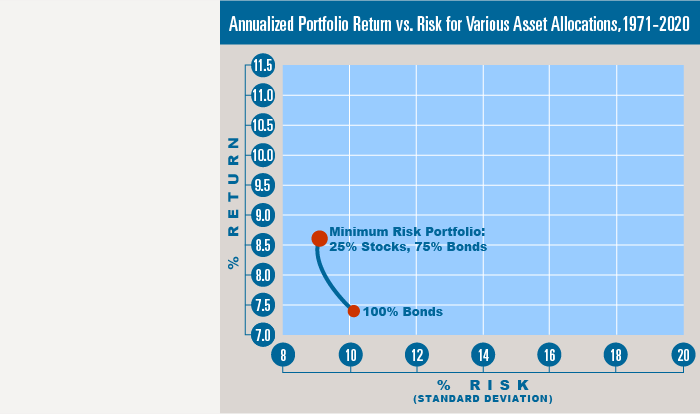

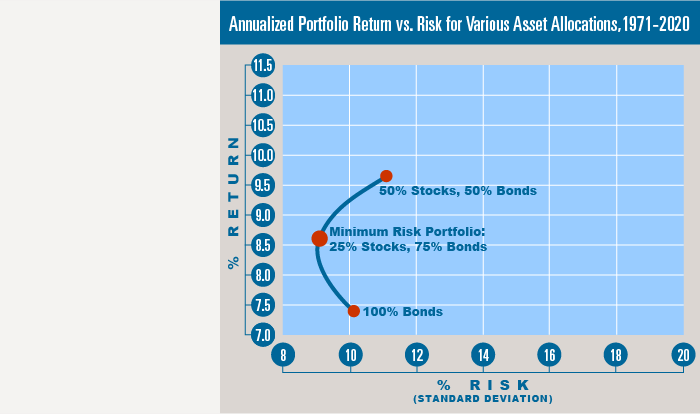

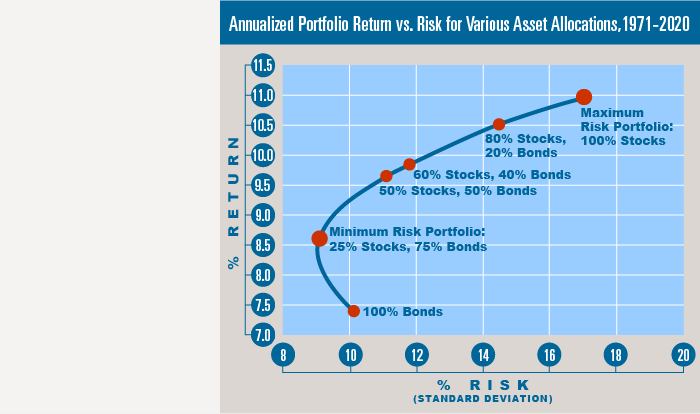

Note that the lowest return portfolio is 100% bonds.

Note that the lowest return portfolio is 100% bonds.

Even though stocks are riskier than bonds, if you blend in a 25% stocks allocation, the portfolio volatility decreases as the return rises.

Note that the lowest return portfolio is 100% bonds.

Even though stocks are riskier than bonds, if you blend in a 25% stocks allocation, the portfolio volatility decreases as the return rises.

Going to 50% stocks did not raise risk much above the 100% bonds allocation, yet it raised annual return more than two percentage points — a huge difference over the fifty year period.

Note that the lowest return portfolio is 100% bonds.

Even though stocks are riskier than bonds, if you blend in a 25% stocks allocation, the portfolio volatility decreases as the return rises.

Going to 50% stocks did not raise risk much above the 100% bonds allocation, yet it raised annual return more than two percentage points — a huge difference over the fifty year period.

Stocks and bonds are largely non-correlated assets — when one zigs, the other often zags. This out-of-sync movement helps stabilize portfolio growth over time.

Because diversification works

Yes, there is such a thing as a free lunch.

Even the simplest diversification, among stocks and bonds, is capable of raising returns while also lowering risk.

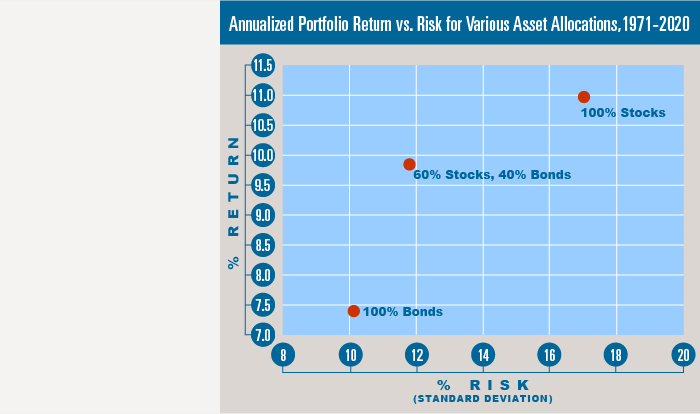

First-level diversification is a start. The 60/40 stock/bond portfolio can be an attractive alternative to an all-stock or all-bond portfolio. However...

First-level diversification is a start. The 60/40 stock/bond portfolio can be an attractive alternative to an all-stock or all-bond portfolio. However...

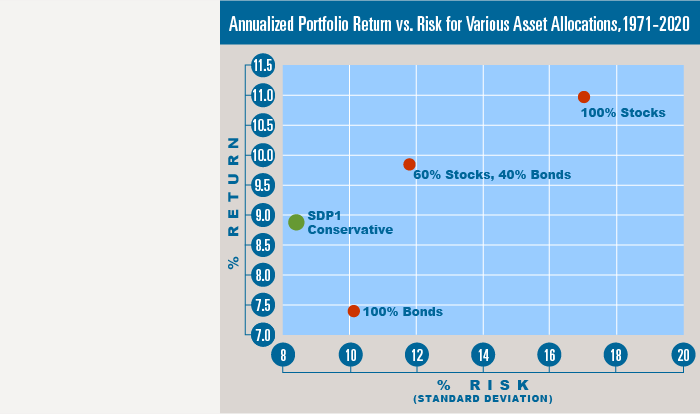

By broadening out the asset allocation, the Conservative SuperD portfolio is a further improvement, with much lower risk than a 60/40 portfolio without sacrificing much return.

First-level diversification is a start. The 60/40 stock/bond portfolio can be an attractive alternative to an all-stock or all-bond portfolio. However...

By broadening out the asset allocation, the Conservative SuperD portfolio is a further improvement, with much lower risk than a 60/40 portfolio without sacrificing much return.

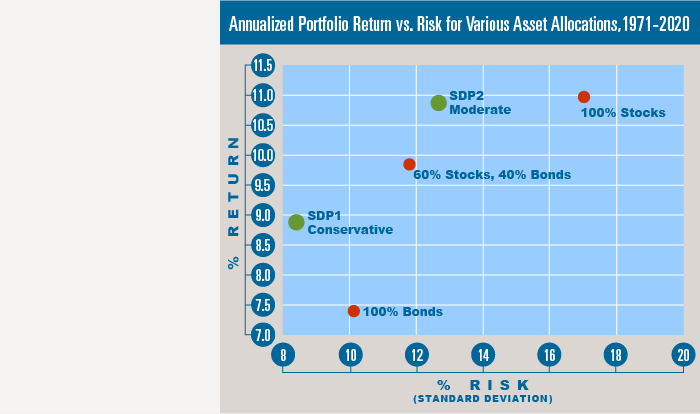

Meanwhile, the Moderate SuperD portfolio has precisely equaled the return of an all-stock portfolio while reducing risk by more than a third.

SuperDiversification works better.

SuperDiversification, or SuperD, takes this effect several steps further.

The magic of broad asset allocation is that you can add riskier assets into a portfolio - and actually reduce the risk of the portfolio!

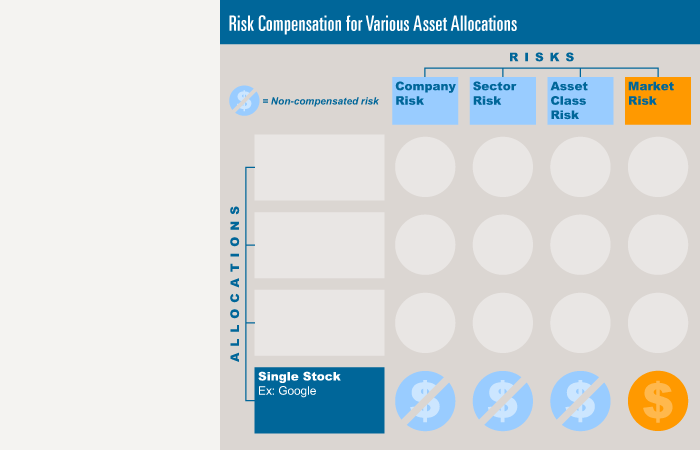

Too many portfolios focus on only one stock or a handful. They take on the risk of the company, its industrial sector, and its asset class — as well as general market risk.

Too many portfolios focus on only one stock or a handful. They take on the risk of the company, its industrial sector, and its asset class — as well as general market risk.

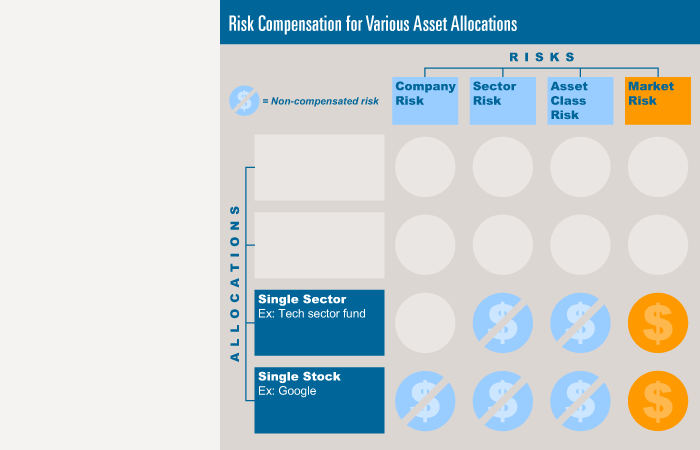

Swapping company stock(s) for a sector fund reduces individual stock risk, but still has the risk of adverse developments in the sector and asset class.

Too many portfolios focus on only one stock or a handful. They take on the risk of the company, its industrial sector, and its asset class — as well as general market risk.

Swapping company stock(s) for a sector fund reduces individual stock risk, but still has the risk of adverse developments in the sector and asset class.

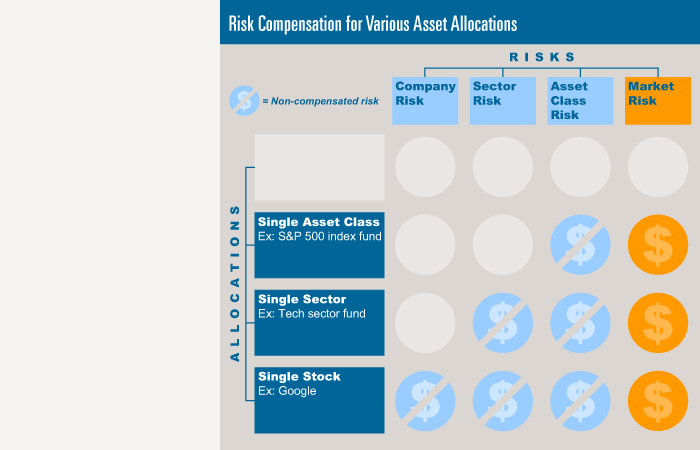

Swapping the sector for a broad asset class fund broadens exposure across many sectors.

Too many portfolios focus on only one stock or a handful. They take on the risk of the company, its industrial sector, and its asset class — as well as general market risk.

Swapping company stock(s) for a sector fund reduces individual stock risk, but still has the risk of adverse developments in the sector and asset class.

Swapping the sector for a broad asset class fund broadens exposure across many sectors.

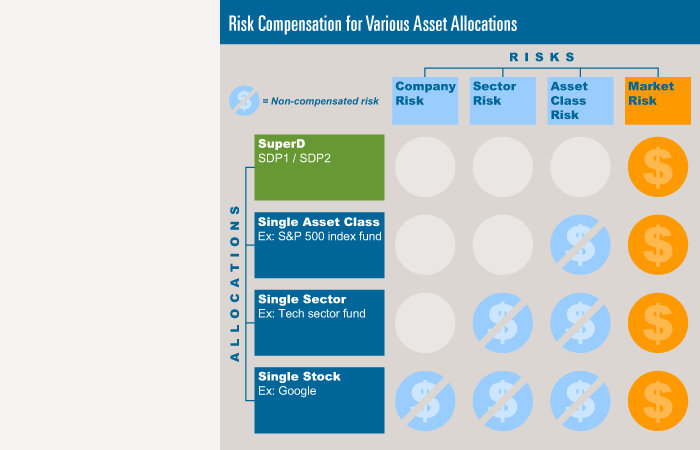

Only a portfolio comprised of many asset classes, such as SuperD has, can reduce asset class risk to the “sleeping point” — leaving only the risk of general market volatility which is inherent in investing.

SuperD seeks to take only the risks you get paid to take.

When you overly focus your portfolio, you take on a set of risks for which you don’t receive adequate — or most often any — compensation.

Only by diversifying broadly can you reduce those uncompensated risks to the vanishing point.

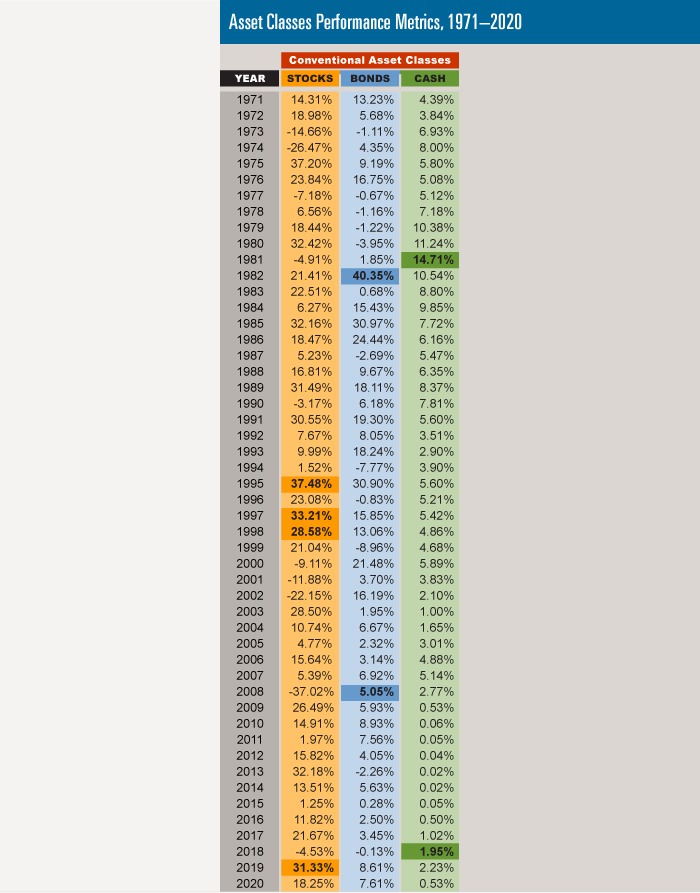

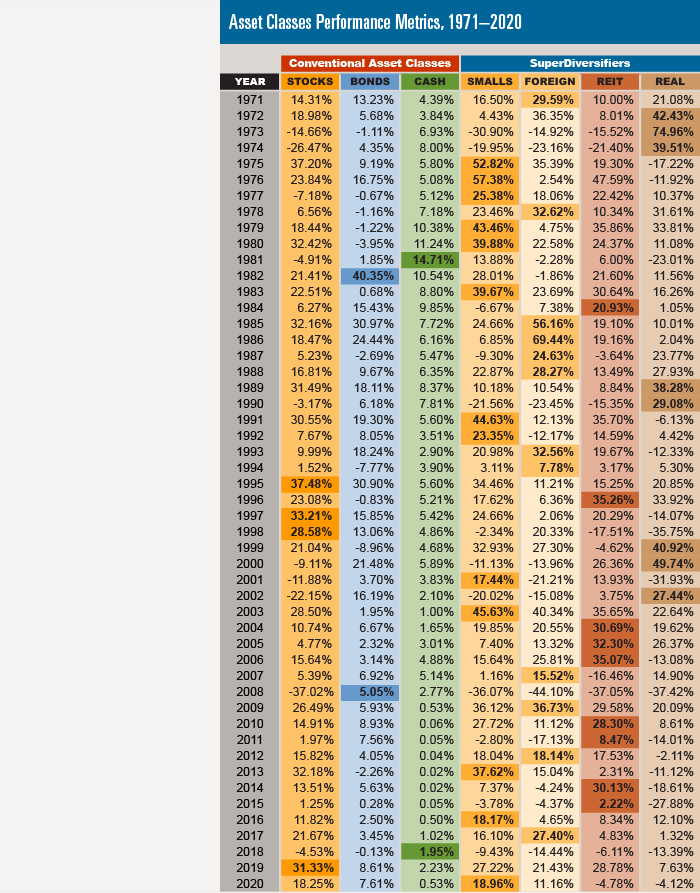

The conventional asset classes (CAA) comprise just three of the seven asset classes we use in our SuperDiversified portfolios. From 1971 through 2020, a span of 50 calendar years, these three conventional asset classes were the standouts in just 8 years.

The conventional asset classes (CAA) comprise just three of the seven asset classes we use in our SuperDiversified portfolios. From 1971 through 2020, a span of 50 calendar years, these three conventional asset classes were the standouts in just 8 years.

By contrast, in 42 of these 50 calendar years — including 19 of the past 22 years — a SuperDiversifier was the top-performing asset class of the year.

Why seven asset classes?

The SuperDiversifiers are often front-runners…

… because there’s always a bull market somewhere.

A SuperDiversifier has been the #1 asset class in 42 of the past 50 years.

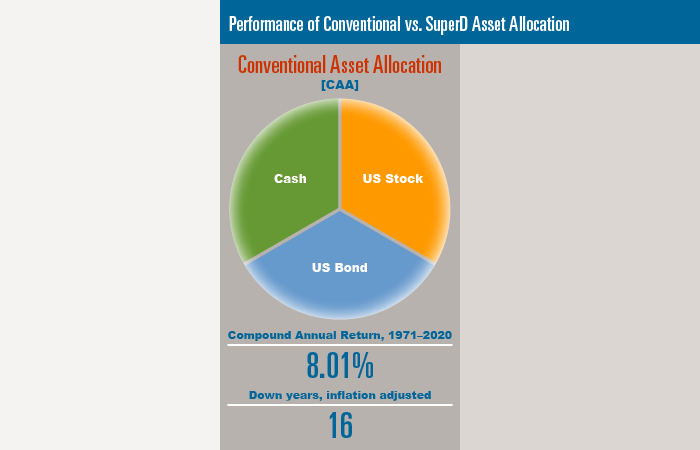

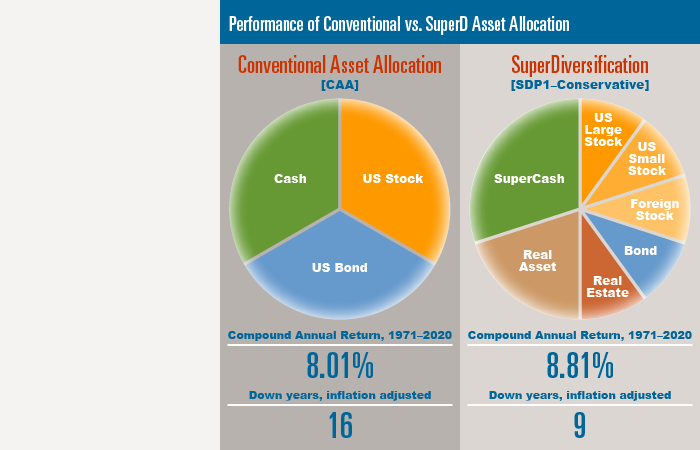

Conventional asset allocation (CAA) has been a kind of standard diversification schema for individual and institutional investors alike for the past five decades. It has done “well enough”, but conservative investors may balk at having lost real wealth in nearly one-third of the past 50 years.

Conventional asset allocation (CAA) has been a kind of standard diversification schema for individual and institutional investors alike for the past five decades. It has done “well enough”, but conservative investors may balk at having lost real wealth in nearly one-third of the past 50 years.

But the conservative version of the SuperDiversified portfolio (SDP1) has beaten the return of CAA by 0.8 percentage points per year while lowering risk substantially, with just nine down years in the past 50. In this span, seven asset classes have proven better — and safer — than three.

Yet they can lower risk.

SuperDiversification is capable of raising portfolio returns and lowering risk.